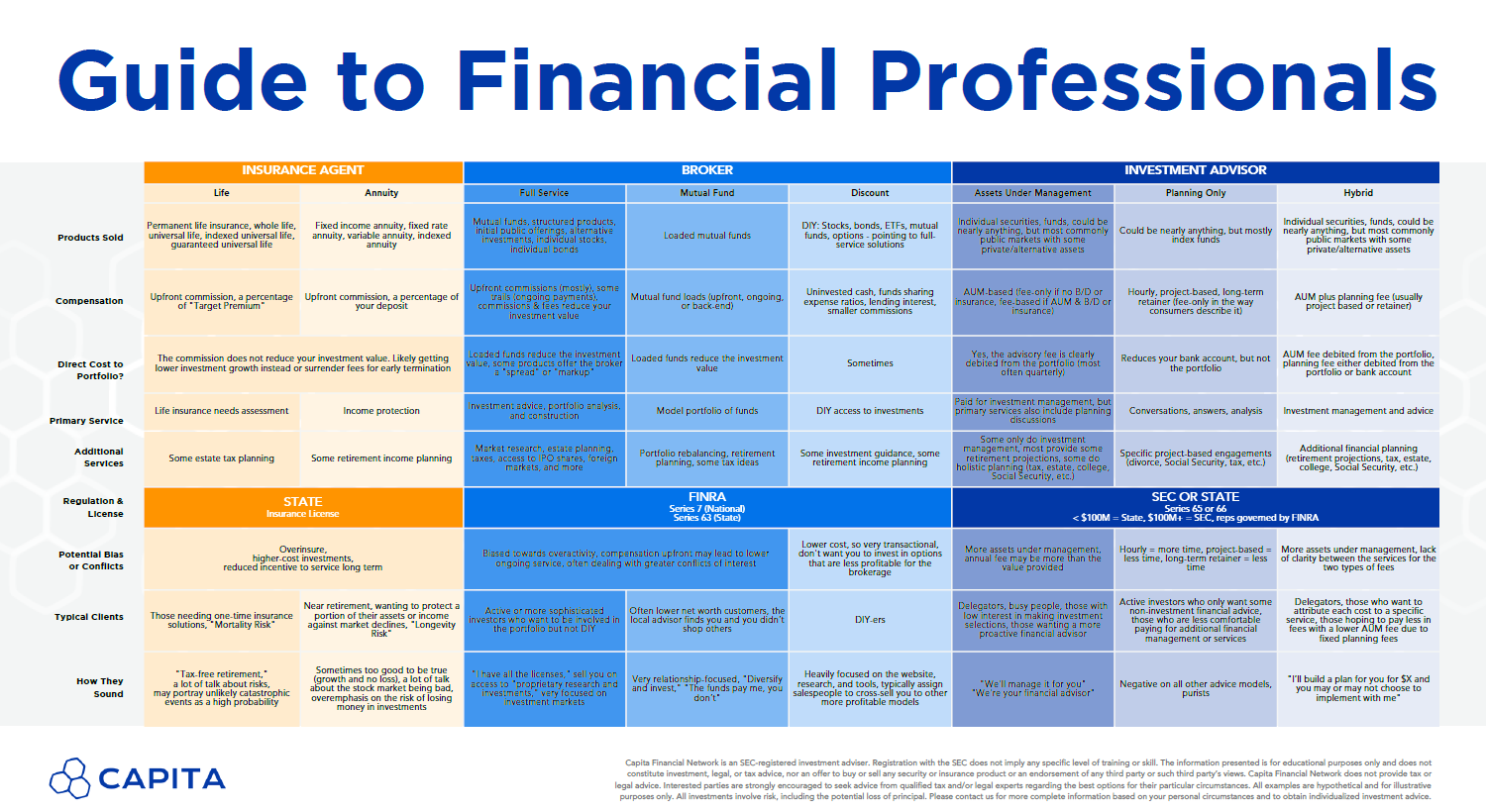

.png)

.png)

Let’s be honest—walking into an advisor’s office armed with a list of 20 probing questions, trying to “catch” them in a lie, isn’t exactly the best way to kick off what should be a lifelong professional relationship. Yet, that’s the advice you’ll often find online. I am an advisor. Let me tell you what an advisor hears, thinks, and knows when you ask these questions:

“Are you a fiduciary?”

“How do you handle conflicts of interest?”

“Do you receive commissions?”

It’s not that these questions are bad or that you don’t deserve transparency. It’s just that a cross-examination approach rarely leads to the kind of conversation that helps you truly understand whether this advisor is a good fit for you.

Because let’s be real—the best financial advisors, the ones who are highly skilled and in demand, don’t have to sit through very many of these kinds of interviews. They get enough referrals from happy clients that they don’t need to convince you of their integrity. If you’re approaching the conversation like a detective interrogating a suspect, you might be missing the bigger picture: What really matters is not whether they say the right things, but whether they demonstrate the right qualities.

That’s where the 4 Cs of Advisor Quality come in. Inspired by the famous 4 Cs of diamond quality, these four traits—Competence, Communication, Care, and Compensation—will help you evaluate an advisor in a way that actually tells you whether they’re a good fit for you.

(Do they actually know their stuff?)

Financial planning isn’t just about picking stocks or running a retirement calculator—it’s about understanding your financial complexity and adjusting as your life changes. So, instead of grilling them about credentials right away, ask questions that reveal their expertise:

The best advisors don’t just recite credentials; they demonstrate their competence through real examples and insights that apply to you.

(Can they explain things in a way that makes sense to you?)

Ever had a conversation with someone who throws out so much jargon you start questioning your own intelligence? Or worse, someone who speaks in a condescending tone, as if you should already know how a backdoor Roth conversion works?

A good financial advisor should be able to explain complex topics in a way that makes sense to you, without making you feel dumb. Pay attention to:

If you walk out of the meeting feeling more confused than when you walked in, that’s a red flag.

(Are they truly looking out for your best interests?)

You don’t want an advisor who just checks the boxes—you want one who actually cares about your financial well-being. This goes beyond their legal obligation to be a fiduciary.

Consider:

This is the most risky aspect of your interview. You need to know their intentions without unintentionally signaling you are a difficult client. Let’s face it, good advisors have options. Sometimes, they have wait lists. You are in a dance. I’m going to teach you how not to misstep on the first note.

You could have asked, “Are you a fiduciary?” But do you really know what that means? What would you do with a “Yes” or “No?” It terrifies me to watch how some clients confidently lower the drawbridge to their net worth castle when I respond “yes” to the fiduciary question. I know too many “fiduciary” wolves for this simple heuristic (rule of thumb) to be sufficient.

Conversely, please don’t trade the fiduciary question for another heuristic. For example, an advisor’s impatience with being interviewed isn’t a sign of success or integrity. How do you think Bernie Madoff would have responded to these questions? Don’t know who Bernie Madoff is? Google it.

Consider this: if someone has the intention of taking advantage of you, the “fiduciary” tag only tells you they are legally required to document a few things before fleecing you.

You want someone who takes the time to understand your values and priorities—not someone who’s just looking to move your money around.

(How do they get paid, and does it align with your needs?)

Let’s not pretend money isn’t a factor here. How an advisor is compensated can influence their advice, so it’s important to understand their business model.

“Can you walk me through your fee structure and what I’d be paying annually?”

“Are there any other costs I should be aware of?”

The less honest advisors will quote you their own fee, but might omit the additional costs to you. After all, they are not charging the additional fees, but that doesn’t matter, it still hits your bottom line.

A good advisor will have no hesitation in explaining how they get paid AND how other fees may apply. If they dance around the question or make it sound unnecessarily complicated, that’s a red flag.

Instead of treating your advisor interview like a courtroom deposition, focus on having a meaningful conversation that helps you assess their Competence, Communication, Care, and Compensation.

A word of warning from my observations in rubbing shoulders with advisors over the years:

Many of the best advisors are not funny, fun, charismatic, good looking or interesting.

Many of the highest paid advisors are funny, fun, charismatic, good looking and interesting.

Be intentional about what you are looking for.

A great financial advisor isn’t just someone who answers all the right questions—it’s someone who makes you feel confident in your financial future. And if you find yourself with an advisor who checks all the boxes, congratulations—you’ve just found the financial equivalent of a flawless diamond.

by Good Riot

by Good Riot

.png)